Introduction

The recent boom in the technology sector has boosted investor confidence, surprisingly given the sector's recent uncertainty, which stems from the AI boom. The AI boom has driven the investor’s optimism, resulting in an enormous surge in investment.

A bellwether stock is a stock that has a very large market cap, where the total value of all the shares is so large that small changes in the company's value would cause a corresponding change in major stock market indexes, such as AAPL in the S&P 500. Two very large bellwether stocks are Tesla and Apple.

Retail investors watch these companies due to their market dominance and their reputation for strong returns. Institutional investors value these companies as indicators of market movement. High valuations can lead to increased investor confidence, stimulating aggregate demand and GDP growth.

Valuation Risks

However, a key question arises— is this growth sustainable, or is it overvaluation? Much of the AI-driven optimism is based on expectations of the market, rather than current profits. Speculative bubbles, like the dot-com bubble and cryptocurrency fluctuations, eventually correct when anticipated profits fall short. Heavy concentration of investment in a few tech companies adds systemic risk, affecting broader markets.

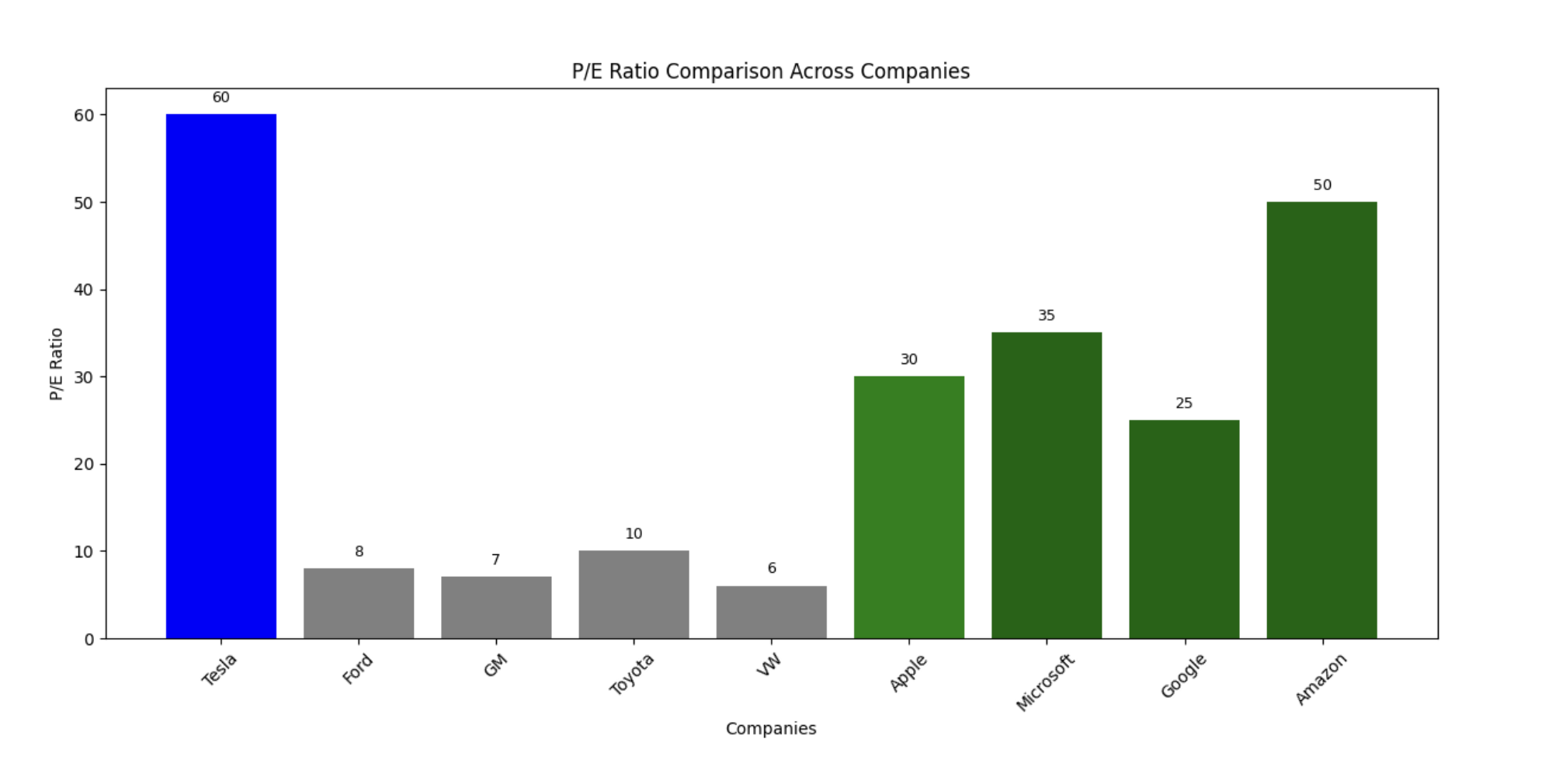

Figure 1: P/E ratio comparison of Tesla and Apple against their respective peers. Tesla trades at a premium relative to legacy automakers, while Apple’s valuation is higher than many tech giants. This visualisation quantifies the investor premiums for growth expectations.

Macroeconomic Influence

The macroeconomic environment is very influential in valuing technology sector investments in several ways. The most crucial determinant is the expected interest rates in the economy. Most technology companies are considered growth companies since they do not make significant profits in the current period but expect to earn considerable amounts of money in the future from innovations. The discounted cash flow technique used to evaluate stock prices will explain why discounting is such a sensitive factor in valuing stocks. Discounting requires estimating future cash flows and then dividing them by the discounting factor. When monetary policy changes show that interest rates are going to fall, then the discount factor becomes smaller, and consequently, the current price rises. Since technology companies have no profit margins, the slightest change in the discount rate can greatly affect their valuations because the future earnings are much higher. When interest falls from, for instance, five per cent to three per cent, then the earnings ten years in the future are increased by more than twenty per cent.

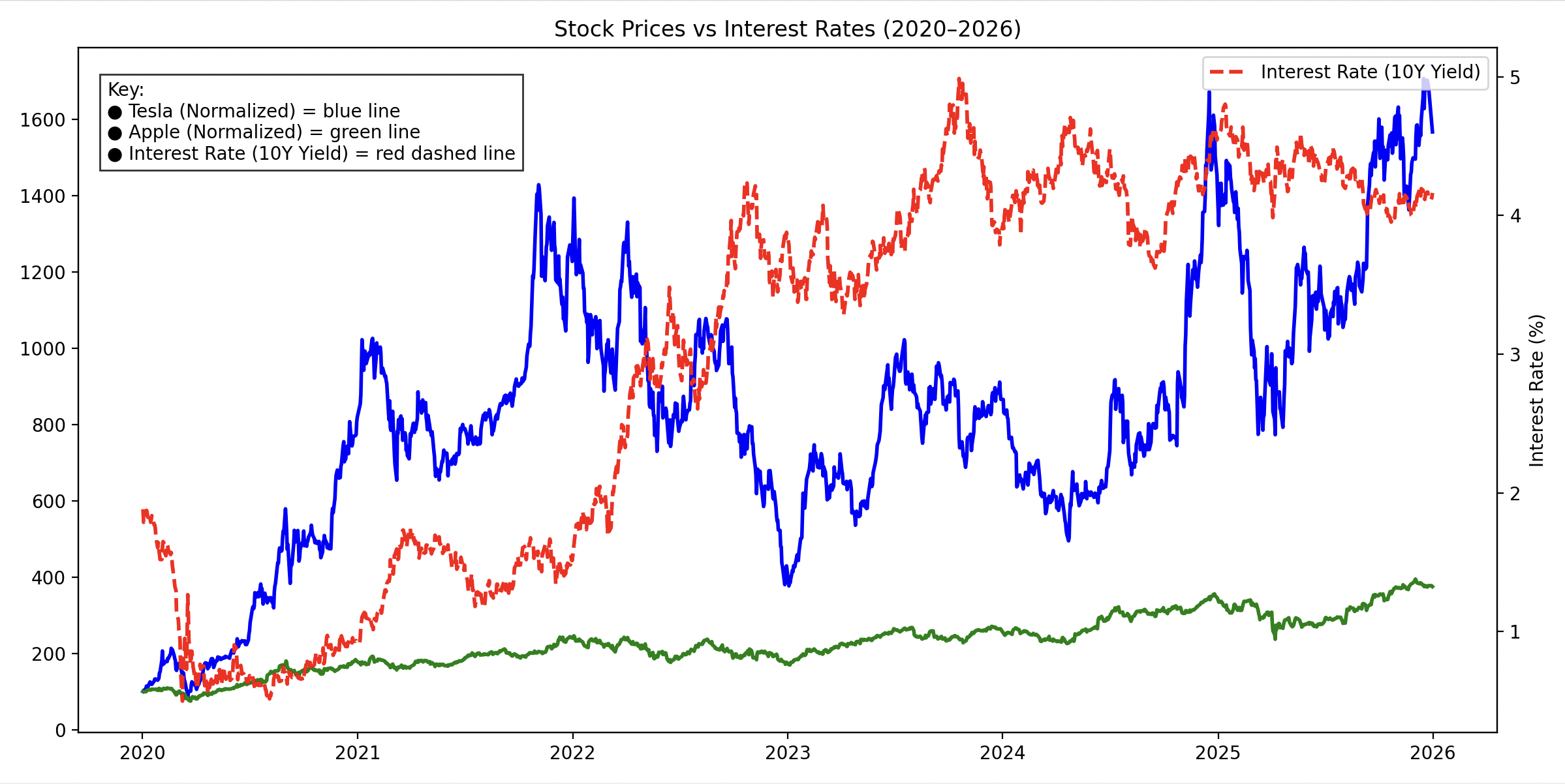

Figure 2: Tesla and Apple’s stock prices respond to changes in interest rates. The blue and green lines show the normalised stock prices of Tesla and Apple, while the red dashed line represents the US 10-year Treasury yield. The graph demonstrates the inverse relationship between interest rates and long-duration growth stock valuations.

The dynamic of inflation impacts valuations in several ways. Low inflation favors equities over fixed income because equities have claims on real assets and real economic capacity whose value is adjusted according to price levels. Too much inflation causes tight money policies, higher discount rates, and lower profit margins due to cost-push and demand-pull factors. The current economic environment is characterised by low but sustained inflation without leading to recession, referred to as the "Goldilocks" environment.

The willingness of investors to take risks, which is determined by macroeconomic factors, also intensifies these effects. When there is an economic upturn and stability in the financial system, investors do not shy away from high-risk and high-yield investments like technology stocks. Market liquidity is another factor that promotes risky behaviour in investors. Central banks' quantitative easing policies add liquidity to the financial markets, reduce risk premiums, and direct capital towards growth stocks. On the other hand, quantitative tightening removes liquidity from the markets, increases volatility, and encourages investors to shift their portfolios to value stocks and bonds. The rise in the popularity of technology stocks recently can be attributed to the expectation of the end of quantitative tightening by the US Federal Reserve and an imminent move towards rate cuts. Investors now expect a shift from quantitative tightening to easing policies. This has fueled investor interest in long-duration growth stocks, providing the necessary macroeconomic backdrop for narratives about innovation in artificial intelligence.

A) Growth Drivers

The valuation of Tesla is based on many different narratives of growth, which go well beyond typical metrics for a traditional car manufacturer. The global market for electric vehicles keeps growing secularly thanks to regulatory forces which push for ending the use of gasoline engines, a trend in consumers' preference towards sustainable technologies, and cost-effectiveness due to reduced prices of batteries. First mover advantages have been achieved by Tesla in terms of integrated manufacturing, proprietary charging stations, and brand value, which its rivals find hard to match.

Nevertheless, it is important to emphasise that the reason behind the high valuation multiple—traditionally operating in the price-to-earnings ratio above fifty compared to the single-digit P/E ratio of traditional car producers—is not related to present sales of cars but optionality in other areas. The story associated with artificial intelligence and self-driving cars is an element of speculation. While the Full Self-Driving feature developed by Tesla may face regulatory and technological challenges, its ability to provide level-five autonomy would change the business model of the company and make it shift from producing cars to becoming a provider of mobility-as-a-service with recurring software revenue streams.

Energy storage and solar systems offer additional avenues of diversification apart from being exposed to automotive sales. The installation of batteries at the grid level tackles the problems of intermittency in renewable energy and puts Tesla in the mega-trend of energy transition. Even though at the moment these industries contribute little to Tesla’s revenues, they grow faster than the car sales industry and possess enormous opportunities for expansion into the future. Brand power makes this even appealing: Tesla enjoys a cult-like fan base that sees it as an innovator and not just a car maker.

B) Risks

The valuation premium embedding these growth narratives creates asymmetric downside exposure should expectations prove overoptimistic. Price-to-earnings multiples of fifty or sixty require sustained hypergrowth to justify—any deceleration in delivery numbers, margin compression, or autonomous driving delays triggers disproportionate valuation contractions. The arithmetic of high-multiple stocks proves unforgiving: a company trading at sixty times earnings that experiences a twenty per cent earnings decline faces mechanical valuation compression of forty-eight per cent merely to maintain the same multiple, before accounting for multiple contraction from disappointed growth expectations.

The biggest and most concrete challenge to Tesla’s position in the market is the increasing intensity of competition. Traditional automobile companies such as Volkswagen, Ford, and General Motors have invested hundreds of billions of dollars in electric cars, using their economies of scale, existing dealership systems, and brands built up over several decades. While it is true that Tesla still enjoys a technological edge in some areas, this is eroded by its competitors’ investments in batteries and software. Chinese car companies are among its strongest competitors, with BYD selling more electric vehicles than Tesla in 2023, thanks to its low cost base, large domestic market size, and government backing.

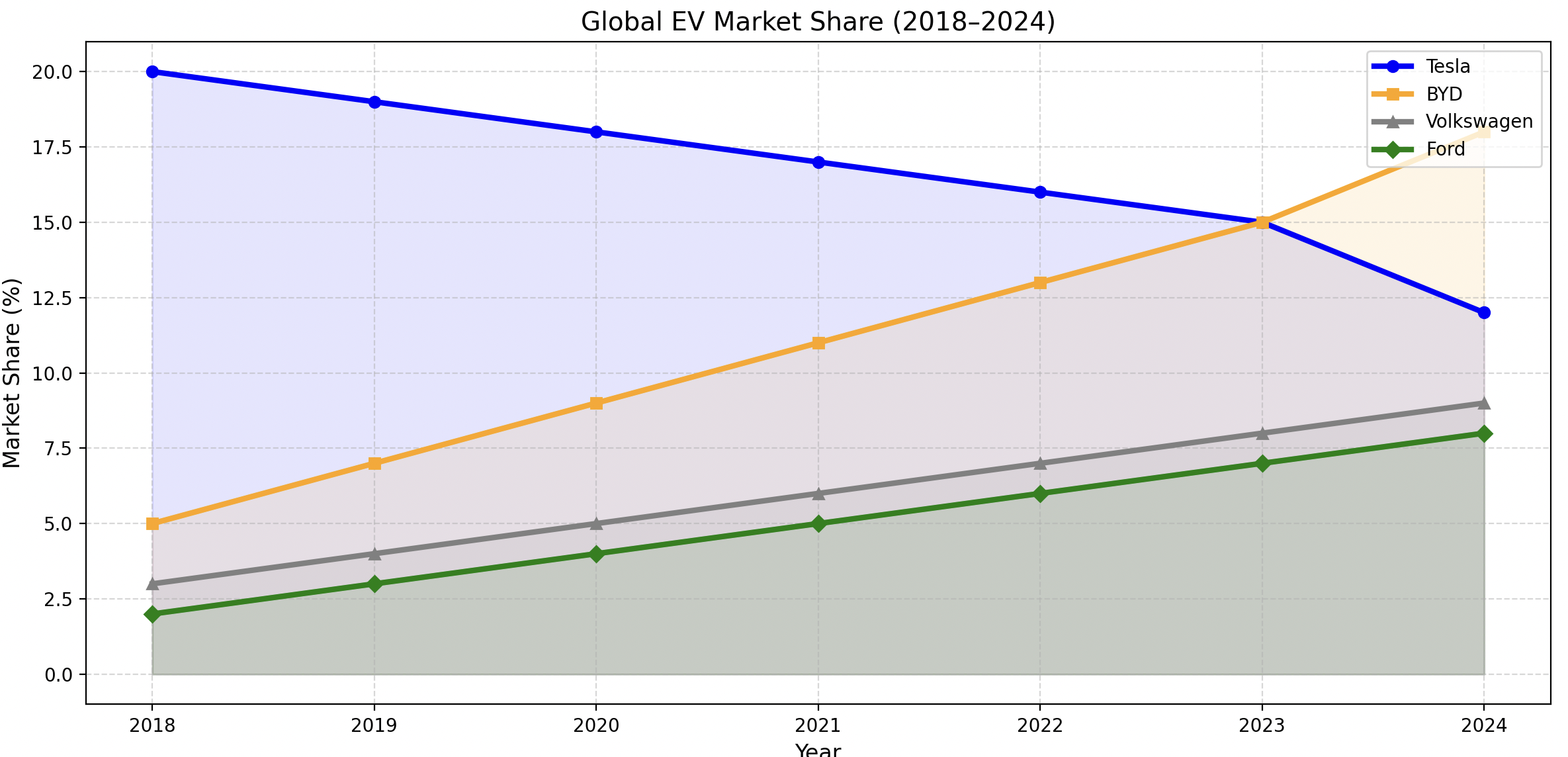

Figure 3: Tesla’s global electric vehicle market share compared with its major competitors. While Tesla continues to grow in absolute sales, its relative market share is declining due to the rapid expansion of companies like BYD, Volkswagen, and Ford. This visualisation highlights the competitive pressures and potential erosion of Tesla’s market dominance.

Regulatory uncertainties compound these competitive pressures. Autonomous driving faces approval processes across multiple jurisdictions, each imposing distinct technical requirements and safety thresholds. The timeline for achieving full regulatory clearance for unsupervised self-driving remains uncertain, potentially extending years beyond current market expectations. Furthermore, subsidy regimes supporting EV adoption face political vulnerability: changes in government priorities could eliminate tax credits and purchase incentives that currently stimulate demand, whilst protectionist measures—tariffs, local content requirements—threaten Tesla's globalised supply chains and export strategies.

Sustainable profit margins are likely the single biggest financial risk. In a situation where there is less competitive pressure from other companies making EVs, Tesla was able to earn operating margins that were the best in the business, thanks to pricing power. With increasing competition requiring Tesla to lower prices to sustain its sales growth rate, margins will come under structural pressure. In addition, the firm needs to allocate significant resources towards developing new technology, driverless cars, and expanding its manufacturing capacity, which will limit cash flow generation.

Whereas Tesla embodies one end of the technology spectrum, Apple epitomises the other end – that of large caps with stable income generation and positive fundamentals. One of Apple’s strengths comes down to lock-in effects from its product ecosystem. This means that their hardware, software, and services generate recurrent revenue as customers do not churn easily due to integration. Furthermore, there have been solid earnings generated in Apple’s services division through offerings like music, cloud computing services, and app store services. These are very profitable and stable sources of revenue that add to overall profitability, in contrast to more volatile revenues from the company's hardware business.

The financial stability of Apple can be seen by their healthy cash flow and cash reserves, which allow it to fund research and development in new projects and acquisitions while being protected in periods of economic instability. Another strength for Apple lies in regular share repurchases that lead to stock stability and returns of capital to stakeholders. Overall, Apple is a defensive growth stock.

Yet, there are some risks associated with Apple's strategy. First of all, a substantial share of income comes from sales of iPhones, which exposes the firm to changes in consumer preferences. Secondly, the market is saturated in many developed countries, limiting opportunities for further growth. Furthermore, the risk of investigation into issues related to antitrust concerns and privacy regulations can be seen as a threat. The upside of Apple is also relatively lower compared to other highly volatile growth stocks like Tesla due to its large-cap status. Despite all risks, Apple’s ecosystem benefits, predictable income, and conservative financial policy make it a solid company to rely on.

Growth Vs Sustainability

The comparison between Tesla and Apple reveals the challenges associated with high potential versus stability. For one thing, Tesla is associated with high beta – its stock price depends on the prevailing market conditions, news and developments, etc. The volatility associated with the company results from market anticipation regarding future changes that could come into place due to innovations in the automotive industry, batteries, and self-driving cars, among others. On the other hand, Apple provides relatively steady returns due to the diversification of revenue sources, which means low volatility.

Finally, there is a difference in the sources of income for Tesla and Apple. While Tesla relies primarily on automotive sales along with options associated with software and energy production, Apple enjoys a consistent source of revenue in terms of several hardware products and services. In turn, such features affect the types of investors interested in investing in Tesla and Apple. Valuation metrics further highlight this difference. The valuation of Tesla operates at a relatively high multiple level due to its high growth and technology options. In the case of Apple, despite being high compared to its historical levels, it has been consistent with the earnings and cash flows generated by the company. The difference between these two valuations can be seen from the P/E ratio comparison shown in Figure 1.

Is this a Bubble?

When it comes to whether or not today's valuations in the technology industry represent a bubble, there must be a careful balance struck between hope in innovations and fundamentals. The valuation of Tesla, for instance, continues to be quite high based on P/E ratios and enterprise value multiples, signalling the fact that investors are pricing in significant growth potential. Although Apple's valuation has been higher than historical levels, it is much more grounded in fundamentals like consistent earnings and cash flow.

There has been a lot of investor excitement related to the concept of artificial intelligence, and its role in technological innovation has caused valuations to rise further, despite the absence of revenues. This represents a case where sentiment has outpaced fundamentals, resulting in a situation that could lead to an eventual correction when market conditions revert to fundamentals.

The risk is evident for Tesla’s competitive advantage. While Tesla is still growing in size, its relative advantage in the electric vehicles sector is eroding because of increased competition from rivals that have scaled their production and made improvements. The decline in Tesla’s global EV market share is depicted in Figure 3, while firms like BYD, Volkswagen, and Ford have grown exponentially. The above observation implies that even though there is growth in the industry, the competitive advantage of Tesla may be under threat in the long term.

Additionally, Figure 2 depicts the effect that the economic environment has on technology stocks, illustrating the inverse correlation between interest rate levels and equity prices. High-growth businesses such as Tesla are exposed to rising discount rates because valuations are dependent on future cash flows. Given Tesla’s intense competition and high market expectations, there is a risk that valuations will be compressed if the projected growth is not realised.

Conclusion

The technology sector continues to dominate in markets and global innovation. However, even the most innovative firms can be overvalued based on their fundamentals, emphasising the need to understand valuation. It is vital to factor in both risk tolerance and strategy when choosing investments. Firms such as Tesla with high beta values present high risk and high returns, while Apple presents stability, cash flows, and modest growth as part of its defensive value growth firm profile.

In long-term technology investment, it is crucial to assess fundamentals, market positioning, and market sentiments associated with the technology industry. The continued rise in technological advancements cannot undermine the need for sound investment strategies that include considerations from a broader perspective.

Back to Homepage